Most California families think about life insurance and estate planning as two separate things. You buy a policy from an insurance agent. You create a trust with an attorney. They sit in separate folders and never really interact.

That approach leaves money on the table and more importantly, it leaves your family exposed to problems that a little coordination would have prevented entirely.

This guide explains exactly how life insurance fits into a California estate plan, what happens when it isn’t structured correctly, and the specific steps that make the two work together the way they’re supposed to.

THE SHORT VERSION

Life insurance is not a substitute for a living trust. But when your policy is properly coordinated with your trust, it becomes one of the most powerful tools in your estate plan delivering immediate, private, court-free funds to your family exactly when they need them most.

Life Insurance Is Not a Replacement for an Estate Plan

I want to address the most common misconception first, because it causes real harm to California families.

Life insurance pays a death benefit when you die. That is valuable. But a life insurance policy even a large one does not:

- Transfer your home or real estate to your family

- Provide instructions for how your assets are managed or distributed

- Protect your family during your incapacity while you’re still alive but unable to manage your finances

- Avoid probate on your other assets

- Name a guardian for your minor children

A revocable living trust does all of those things. Life insurance, properly structured, works alongside your trust not instead of it.

Think of it this way: your trust is the framework that governs everything you own. Your life insurance policy is one of the assets that flows into that framework when the time comes. Getting that flow right is what this guide is about.

Why the Beneficiary Designation on Your Policy Matters More Than You Think

When you sign a life insurance policy, you name a beneficiary. That designation not your will, not your trust controls where the death benefit goes. Most people fill it in once when they buy the policy and never think about it again.

That single form can cause serious problems if it isn’t reviewed as part of your overall estate plan.

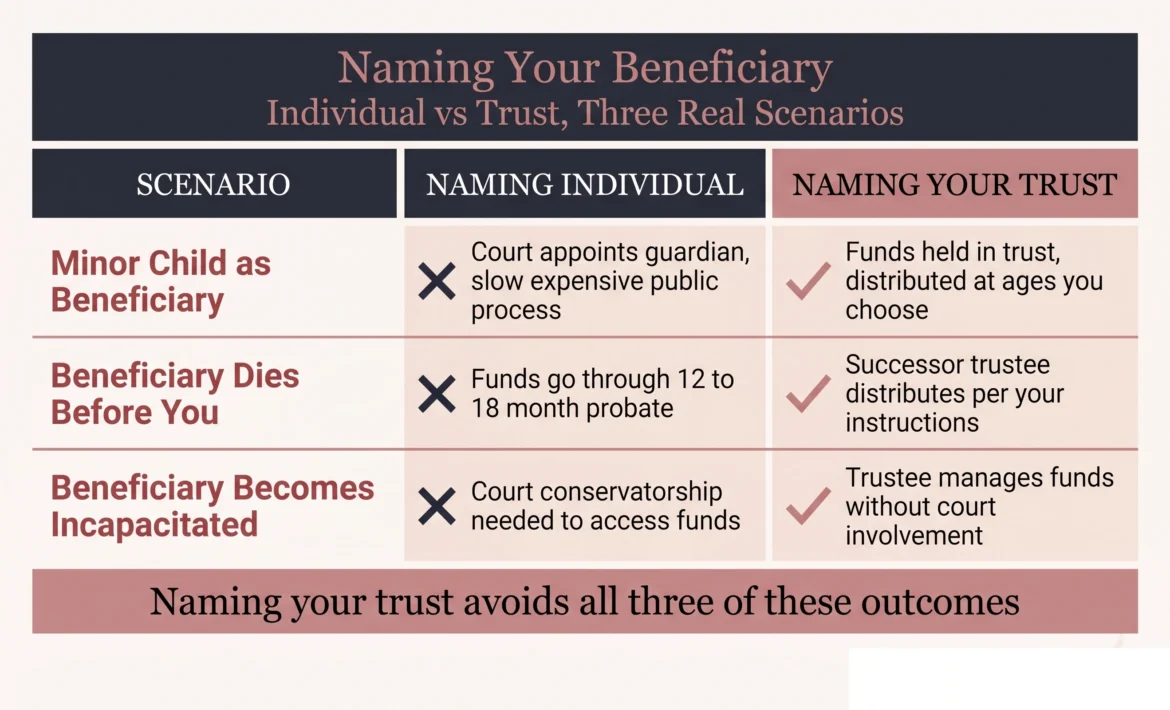

The Problem With Naming a Minor Child Directly

California law does not allow minors to receive life insurance proceeds directly. If you name a child under 18 as your beneficiary and you pass away, a court must appoint a guardian of the estate to manage those funds a process that is slow, expensive, and very public.

The court, not you, controls how the money is managed until your child turns 18. At 18, your child receives the entire amount at once, with no conditions and no guidance. That is almost never what parents intend.

The Problem With a Named Beneficiary Who Passes Before You

If your named beneficiary dies before you and you haven’t updated the designation, the proceeds may be paid to your estate which means they go through probate. The private, immediate transfer you expected from your life insurance policy suddenly becomes a 12 to 18 month court process.

The Problem With an Incapacitated Beneficiary

If a named beneficiary becomes incapacitated before or at the time of your death, distributing funds directly to them may be legally complicated or impossible without a conservatorship again, a court process you were trying to avoid.

How to Name Your Trust as Beneficiary and Why It Works

When your trust is the named beneficiary of your life insurance policy, the death benefit flows directly into the trust. Your successor trustee receives those funds and distributes them according to the exact instructions you wrote privately, immediately, and without court involvement.

This gives you control that a simple beneficiary designation can never provide:

- Funds can be held in trust for minor children until a specific age 25, 30, or a milestone of your choosing

- You can direct that funds be used for specific purposes education, housing, healthcare before general distribution

- You can stagger distributions over time rather than delivering a lump sum

- You can account for beneficiaries with special needs without disqualifying them from government benefits

The Three-Step Process

Step 1: Make sure your trust is fully drafted and signed. You cannot name a trust as beneficiary until it exists as a legal document.

Step 2: Contact your insurance company and request a beneficiary change form. The designation line should read: ‘[Your Name], Trustee of the [Trust Name], dated 2026, or successor trustee.’ Your attorney can confirm the exact language.

Step 3: Confirm the change in writing. Request a confirmation letter or updated policy documents showing the trust as the named beneficiary. Do not assume the change was processed verify it.

|

Life Insurance at Every Stage: How the Role Changes

The reason life insurance matters ‘at any age’ as the original version of this post noted is that what the policy is doing for your estate plan shifts significantly over time. Here is how that actually breaks down for California families.

| Life Stage | Primary Estate Planning Concern | How Life Insurance Fits |

| Young family (20s–30s) | Income replacement + minor children | Death benefit funds trust for children’s care; avoids court guardianship of estate |

| Established homeowner (40s–50s) | Home equity, retirement savings, dependent children still in school | Provides liquidity for family during trust administration; covers mortgage if needed |

| Pre-retirement (late 50s–60s) | Asset transfer, blended family considerations, aging parents | Equalizes inheritances between heirs; funds trust for a surviving spouse |

| Retirement (65+) | Probate avoidance, incapacity planning, legacy goals | Funds trust for final expenses and estate costs; preserves other assets for heirs |

The mechanics of how life insurance interacts with your trust remain the same across all of these stages. What changes is the size of the policy, the purpose of the proceeds, and how the distribution instructions in your trust are written. All of it should be reviewed together as one coordinated plan.

A California-Specific Note on Community Property and Life Insurance

California is a community property state, which means assets acquired during marriage including life insurance premiums paid with marital income are generally owned equally by both spouses.

This matters in a few specific ways:

- If you purchased a life insurance policy during your marriage using community funds, your spouse may have a community property interest in that policy even if you are the named owner.

- Changing the beneficiary of a community property policy without your spouse’s written consent may not be valid under California law.

- When coordinating life insurance with your trust, how you title the policy and the trust should be reviewed together, especially if you have a blended family or are in the process of updating an existing plan after a life change.

This is not a reason to avoid naming your trust as beneficiary it is a reason to make sure the coordination is done correctly, with an attorney who understands both your trust structure and California’s community property rules.

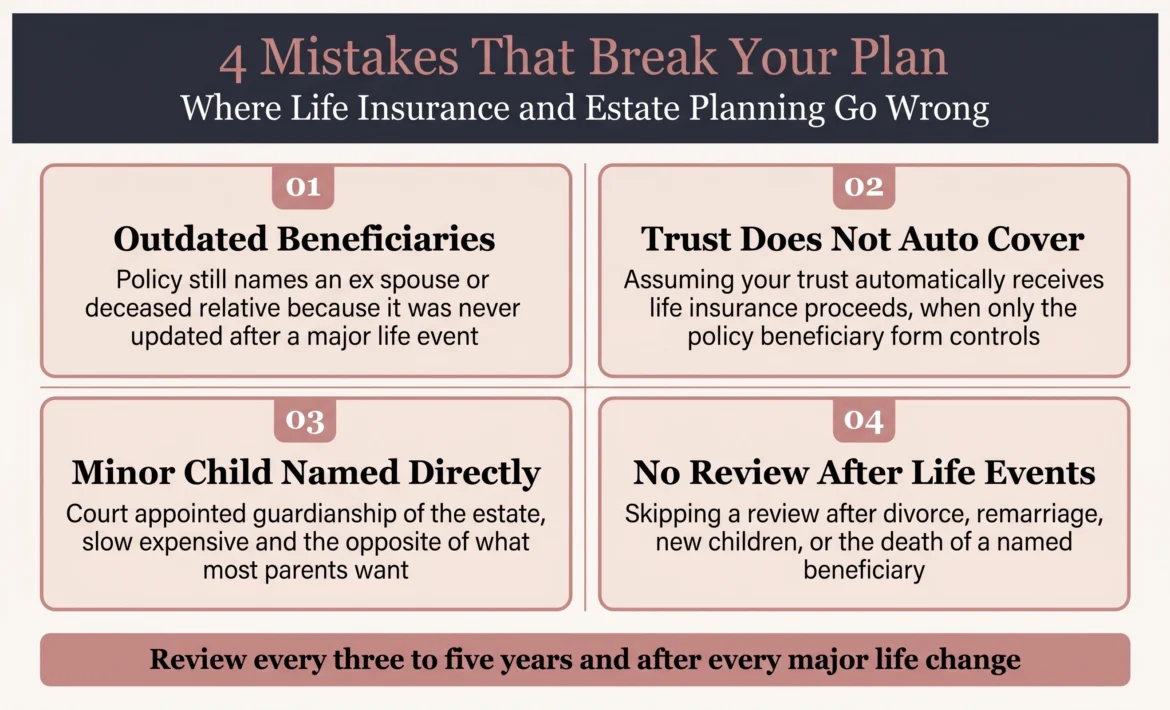

The Most Common Mistakes We See

Buying a Policy and Never Updating the Beneficiary

A policy purchased before you had children, before you created your trust, or before a divorce or remarriage almost certainly has an outdated beneficiary designation. The policy is only as useful as the name on that form. Review it every time your estate plan is updated which should be every three to five years and after every major life change.

Assuming the Trust ‘Automatically’ Covers Life Insurance

A trust does not automatically capture life insurance proceeds. The policy’s beneficiary designation controls the distribution not your trust document. Your trust must be explicitly named as the beneficiary on the policy for the proceeds to flow into it.

Naming a Minor Child Directly

As described above: California courts will not distribute life insurance proceeds directly to a minor. The result is a court-supervised guardianship of the estate that lasts until the child turns 18 the opposite of what most parents want.

Not Reviewing After a Major Life Event

Divorce, remarriage, a new child, the death of a named beneficiary, or a significant change in your estate’s value are all triggers to review your beneficiary designations. This review should happen at the same time you review and update your trust.

Frequently Asked Questions

Should I name my trust or my spouse as the beneficiary of my life insurance?

It depends on your family’s situation and how your trust is structured. Many married couples name their spouse as primary beneficiary and the trust as contingent beneficiary so the surviving spouse receives funds directly, and the trust governs distribution only if both spouses pass at the same time or the spouse is no longer living. Families with minor children, blended family considerations, or large policies often benefit from naming the trust as primary. This is a decision to make with your estate planning attorney as part of reviewing your complete plan.

What happens if I die before updating my life insurance beneficiary to my trust?

If an individual is named as beneficiary, that person receives the proceeds directly outside your trust and without the distribution controls you wrote into it. If the named beneficiary is a minor, a court proceeding will be required. If the named beneficiary predeceased you and no contingent beneficiary is named, the proceeds may be paid to your estate and go through probate. Keeping your beneficiary designations current is one of the most important maintenance tasks in any estate plan.

Does life insurance go through probate in California?

Life insurance with a named living beneficiary does not go through probate it transfers directly to that person. However, if no living beneficiary exists (because both the primary and contingent beneficiaries predeceased you, or because none was named), the proceeds are paid to your estate and become subject to probate. Naming your trust as beneficiary or maintaining current primary and contingent beneficiaries prevents this outcome.

Can I change my life insurance beneficiary to my trust after the trust is created?

Yes. Contact your insurance company and request a beneficiary change form. Name the trust using the precise legal language your attorney provides. Once submitted and confirmed in writing, the trust is the named beneficiary. This change does not affect your coverage, your premiums, or any other terms of the policy. It is a simple administrative update and one of the most important steps in coordinating your insurance with your estate plan.

Is Your Life Insurance Working With Your Estate Plan or Against It?

At the Law Office of Ishajeet K. Singh, APC, we review your life insurance beneficiary designations as part of every

complete estate plan

A policy that isn’t coordinated with your trust can undo years of planning in a single form.

Schedule Your Free Consultation →

Virtual appointments available statewide. No obligation. No pressure.

This article is for general informational purposes only and does not constitute legal advice. For advicespecific to your situation, please consult with a licensed California estate planning attorney.