If you’re asking this question, you’re probably trying to figure out whether a life estate is the right tool for your family’s situation – or whether something like a living trust would serve you better. As a California estate planning attorney serving families throughout the San Fernando Valley, I find that life estate questions almost always end up in the same place: a trust turns out to be the better option for most homeowners.

But that doesn’t mean life estates aren’t worth understanding. In the right circumstances they’re a useful tool, and if a parent, an attorney, or a financial advisor has brought one up in your planning conversations, you deserve a clear explanation of how they work – and when they don’t.

This post explains who owns property in a life estate, how rights and responsibilities split between the parties, and why I typically recommend a revocable living trust instead for most California families. By the end, you’ll have enough information to make a confident decision – or to come to a consultation already knowing the right questions to ask.

Not Sure Whether a Life Estate or Living Trust Is Right for Your Family?

This is exactly the kind of question I work through with families in a free 30-minute consultation, no legal jargon, no pressure, just a plain-English answer for your specific situation.

Schedule Your Free Consultation →

Virtual appointments available statewide. No obligation. No pressure.

Quick Answer

In a life estate, two parties share ownership simultaneously: the life tenant holds the present right to use and occupy the property during their lifetime, and the remainderman holds the future interest – automatic full ownership that activates at the life tenant’s death.

Major decisions like selling or refinancing require both parties’ consent, because both hold legally enforceable interests in the property.

For most California homeowners, a revocable living trust accomplishes the same probate-avoidance goals as a life estate – with significantly more flexibility, fewer legal complications, and stronger protection if your circumstances change.

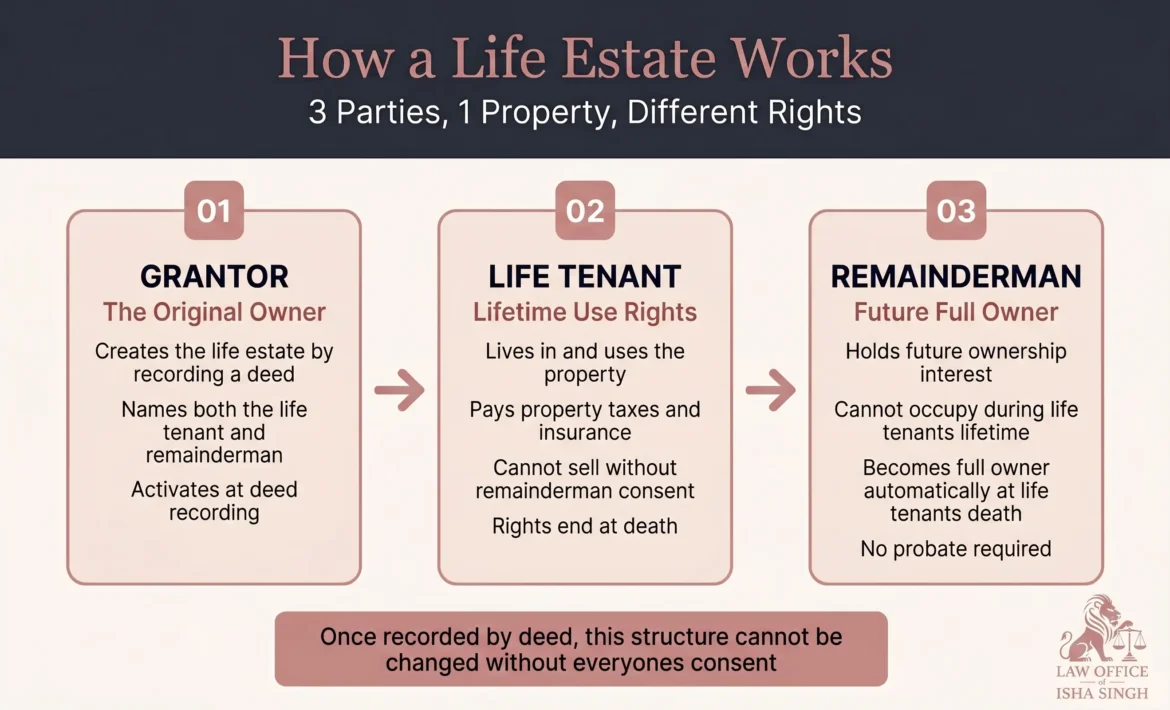

1. What Is a Life Estate?

A life estate is a property ownership arrangement that splits one property into two simultaneous ownership interests. The life tenant – often the original property owner – retains the right to live in, use, and receive income from the property for the rest of their life. When the life tenant dies, ownership automatically transfers to the remainderman (the named heir) without going through probate court.

Here’s how the three parties in a life estate relate to each other:

| Party | Role | When rights activate |

| Grantor | The original property owner who creates the life estate by deed | At deed recording |

| Life tenant | Person with lifetime use rights (often the grantor themselves) | Immediately upon recording |

| Remainderman | Person who inherits full ownership automatically | Upon the life tenant’s death |

California law requires life estates to be created through a written, recorded deed. Oral agreements are unenforceable under the California Statute of Frauds. The deed must clearly identify the life tenant, the remainderman, and the property’s complete legal description.

2. Rights and Responsibilities of Each Party

The ownership split in a life estate creates a clear division of rights and responsibilities. Understanding this division matters because it shapes everything from day-to-day property management to what happens if either party wants to sell.

Rights

| Right | Life tenant | Remainderman |

| Possession and use | Full right to live in, rent out, or use the property during lifetime | No right to occupy while the life tenant is alive |

| Income | May collect rental income or other profits from the property | None until the life tenant’s death |

| Sale or refinancing | Cannot sell or refinance without the remainderman’s consent | Holds future ownership but no right to force a sale while life tenant lives |

| Ownership after death | Interest ends at death | Becomes full owner automatically – no probate required |

Responsibilities

| Responsibility | Life tenant | Remainderman |

| Property taxes | Responsible for all property taxes | No contribution required |

| Insurance | Must maintain homeowner’s insurance | No obligation during life tenant’s lifetime |

| Maintenance | Must maintain the property and prevent “waste” | Can inspect property and sue for waste if value is damaged |

What Is “Waste” – and Why It Matters

In real estate law, “waste” occurs when a life tenant’s actions – or deliberate neglect – substantially reduce the property’s market value. California courts define waste as failing to act as an “ordinarily prudent person” would in caring for their own property.

Common examples include unpaid property taxes that lead to liens, deferred maintenance causing structural damage, removing valuable fixtures, or allowing the property to become uninhabitable. The remainderman has the right to sue for waste while the life tenant is still living – which is one of several reasons life estates can create family conflict that a trust typically avoids.

3. How a Life Estate Is Created in California

A life estate is created by recording a deed that contains the appropriate language identifying the life tenant and remainderman (for example: “to Jane for life, then to Raj”). The deed must be notarized and recorded with the county recorder’s office where the property is located.

This sounds straightforward, but in practice it requires careful attention to California’s specific legal requirements. The deed must include the exact legal property description, comply with recording format requirements, and be structured in a way that doesn’t inadvertently trigger adverse Prop 13 or Prop 19 consequences. A deed that’s improperly drafted – or one that doesn’t account for your existing mortgage’s due-on-transfer clause – can create serious problems that are difficult and expensive to undo.

This is one of the reasons I’d encourage anyone considering a life estate to work with a California-licensed estate planning attorney rather than using an online form. The upfront cost of getting it right is far lower than the cost of untangling a mistake after the fact.

4. Benefits of a Life Estate

When structured correctly and used in the right circumstances, life estates offer several genuine benefits.

Probate avoidance

Because the remainderman’s ownership interest is established by deed – not by a will – the property transfers automatically at the life tenant’s death without going through California’s probate process. This is the primary reason families consider them.

Medi-Cal planning

Life estates can be used as part of a Medi-Cal planning strategy. California’s Medi-Cal Estate Recovery Program (MERP) recovers costs from probate estates – and a properly structured life estate can potentially keep a home outside the recovery scope. However, this area is highly fact-specific. Timing matters significantly: transfers made within the 30-month look-back period before applying for Medi-Cal long-term care benefits can affect eligibility. This is a situation where working with an attorney who understands both estate planning and elder law is essential.

Tax step-up at death

When the remainderman inherits the property at the life tenant’s death, they typically receive a stepped-up basis under IRS Code §1014 – meaning capital gains tax is calculated from the property’s value at the life tenant’s death, not from its original purchase price. This can represent significant tax savings for heirs of appreciated California real estate.

Protection for blended families

A life estate can ensure that a surviving spouse has the right to remain in the family home for life, while preserving ultimate ownership for children from a prior marriage. This is a common use case in blended family planning, though a trust with carefully drafted distribution provisions often accomplishes the same goal with more flexibility.

Considering a Life Estate for Your Home?

Before creating one, it’s worth understanding whether a living trust would serve your family better. In many cases it does — and a free consultation is the fastest way to find out.

Schedule Your Free Consultation →

Virtual appointments available statewide. No obligation. No pressure.

5. Proposition 19 and Life Estates

This is one of the most important – and most misunderstood – areas of California property law for families with significant real estate.

Proposition 19, which took effect February 16, 2021, dramatically changed the rules around inherited property and property tax reassessment. Before Prop 19, a parent could transfer a home to a child and the child could keep the parent’s low property tax base – regardless of whether they lived there. That unlimited exclusion is gone.

Now, for a child to avoid reassessment on an inherited home, they must move in and use it as their primary residence within one year of inheriting it. The exclusion is also capped: it only shields the amount up to $1,000,000 above the property’s current factored base year value (the cap is adjusted annually for inflation). If the child doesn’t meet these requirements, the property is reassessed at full current market value – which for long-held San Fernando Valley homes can mean a dramatic increase in annual property taxes.

For a family whose parents bought their Chatsworth home in 1988 for $180,000, and that home is now worth $900,000, the difference between a reassessed and unreassessed property tax bill can be meaningful – potentially $6,000 to $10,000 per year or more depending on the specific circumstances.

How your trust or life estate is structured now affects how Prop 19 applies when the property transfers. This is a planning decision that deserves careful attention, and it’s one of the areas where I spend significant time with clients in the San Fernando Valley. Learn more about estate planning and how Prop 19 affects your plan.

6. Drawbacks of Life Estates and Why Many Families Choose a Trust Instead

Life estates have real limitations that often make a revocable living trust the more practical choice for California homeowners. Here’s an honest look at what can go wrong.

Inflexibility once created

Once a life estate deed is recorded, changing it requires the remainderman’s cooperation. If you later want to refinance, sell the property, or change who receives it – perhaps because a named remainderman has a divorce, creditor problems, or a relationship breakdown – you cannot do so without their consent. A revocable trust, by contrast, can be amended by you alone at any time while you are competent.

Reverse mortgage complications

Most reverse mortgage lenders will not issue loans on life estate properties because the life tenant doesn’t hold full legal title. For seniors who may later need to access home equity for care costs, this eliminates a significant option.

Medi-Cal risks if improperly structured

While life estates can be used for Medi-Cal planning, they can also create exposure if not handled correctly. Mistakes in timing, documentation, or structure can leave the property vulnerable to MERP recovery. This area requires specialized guidance – not a general-purpose deed template.

Family conflict potential

Because the remainderman has a legally enforceable ownership interest from the moment the deed is recorded, disagreements between the life tenant and remainderman can become legal disputes. If the life tenant fails to maintain the property, pays taxes late, or attempts to make changes the remainderman objects to, the relationship – and the estate plan – can unravel.

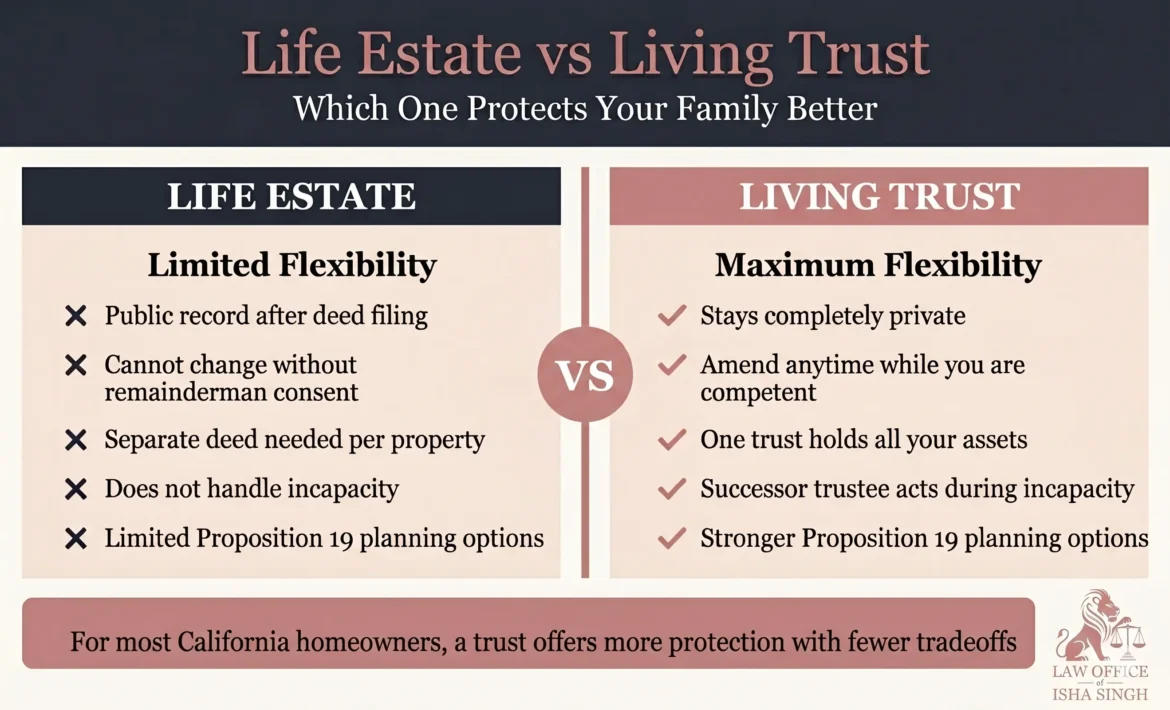

7. Life Estate vs. Revocable Living Trust: Which Is Right for Your Family?

For most California homeowners, a revocable living trust accomplishes everything a life estate does – probate avoidance, direct transfer to named beneficiaries, privacy – with significantly more flexibility and fewer complications. See our detailed guide on how much estate planning costs.

| Life estate | Revocable living trust | |

| Avoids probate | Yes (for that property) | Yes (for all trust assets) |

| Stays private | No – deed is public record | Yes – trust is private |

| Can be changed unilaterally | No – requires remainderman’s consent | Yes – at any time while you’re competent |

| Works for multiple properties | Requires separate deed for each | Yes – one trust holds all assets |

| Handles incapacity | No | Yes – successor trustee acts immediately |

| Prop 19 planning flexibility | Limited | Stronger planning options available |

| Medi-Cal planning tool | Potentially, if properly timed | Generally not – but MERP generally doesn’t apply |

A life estate has a role in specific planning situations – primarily when Medi-Cal timing is a factor and a trust isn’t available as an option. But for the typical San Fernando Valley homeowner who wants to protect their home, name who gets it, and avoid putting their family through probate, a trust is almost always the more practical and flexible choice.

Most California Families Who Ask About Life Estates End Up Choosing a Trust.

A free 30-minute consultation is the fastest way to find out which option is right for your family’s specific situation — no pressure, no legal jargon, just a clear answer.

Schedule Your Free Consultation →

By Zoom or in person | Serving the San Fernando Valley and California statewide

Frequently Asked Questions

What happens if the remainderman dies before the life tenant?

The remainderman’s ownership interest passes through their estate – to their heirs under their will, or under California’s intestate succession laws if they died without a will. This means someone the life tenant never chose could end up as the remainderman. A trust addresses this by allowing you to name alternate beneficiaries.

Can a remainderman force the sale of the property?

Generally no – not while the life tenant is alive. California courts require that a partition sale serve all parties’ best interests, and the life tenant’s right to occupy the property typically takes priority during their lifetime. After the life tenant’s death, multiple remaindermen do have the right to pursue a partition action if they can’t agree on what to do with the property.

Does a life estate protect property from Medi-Cal recovery?

It can – if properly structured and timed. California’s Medi-Cal Estate Recovery Program typically recovers from probate estates, and a properly structured life estate passes outside probate. However, the 30-month look-back period for long-term care benefits means timing matters significantly. Medi-Cal planning is a complex, fact-specific area that requires guidance from an attorney familiar with both estate planning and elder law.

How is a life estate different from a living trust?

A life estate splits ownership of one specific property between two parties – permanently, once the deed is recorded. A revocable living trust is a legal vehicle that holds all of your assets, can be amended or revoked at any time, handles incapacity as well as death, and provides far more flexibility for changing circumstances. For most California homeowners, a trust accomplishes the same probate-avoidance goals with significantly fewer tradeoffs.

Is a life estate deed a public record in California?

Yes. Because a life estate is created by recording a deed with the county recorder, the arrangement – including who the remainderman is – becomes part of the public record. A living trust, by contrast, is a private document that never enters the public record unless it becomes the subject of litigation.

This post is for general informational purposes only and does not constitute legal advice. Reading this post does not create an attorney-client relationship. Estate planning costs vary based on individual circumstances. For a quote specific to your situation, please schedule a consultation. Read our full disclaimer.